How to R - Beginner Guide Time Series Analysis

- Data Science

- beginners guide, forecast, r, time series

- 5 min reading time

Dr. Stefan Lieder

In the tutorial "How to R - Beginner Guide Time Series Analysis", a time series analysis with R is carried out, outlining the essential steps of data preparation, modelling and visualization. The focus is on the use of the R packages tidyverse, tsibble and fable.

Table of contents

Time series analysis with R

In this short tutorial, we will limit ourselves to briefly outlining the essential steps in time series analysis in the R programming language.

These are:

- Data preparation,

- Modeling and

- Visualization.

We use the R packages tidyverse, tsibble and fable for this.

Data preparation

As a rule, all necessary functions for general data preparation are contained in the "tidyverse" package collection. For data preparation in the "tidy" style, however, the "tsibble" package is also needed. First we load the packages and the data:

library(fable)

library(tsibble)

library(tidyverse, quietly = TRUE, warn.conflicts = FALSE)

raw_data = read_delim("~/Documents/Progonosewerkstatt/Peer_Labs/R/2_DataPreparation/01_Data/Company.csv", delim=";")

glimpse(raw_data)

## Rows: 101

## Columns: 9

## $ Month <dttm> 2011-01-01, 2011-02-01, 2011-03-01, 2011-04-01, 2011-05-…

## $ Germany <dbl> 19722000, 25062000, 47066000, 52625000, 66489000, 5660100…

## $ Canada <dbl> 1809000, 2206000, 3035000, 3793000, 4813000, 4370000, 454…

## $ Switzerland <dbl> 3624000, 4972000, 7010000, 7084000, 9452000, 7971000, 733…

## $ Austria <dbl> 1436000, 2390000, 6556000, 7544000, 9069000, 8154000, 817…

## $ US <dbl> 3598000, 3349000, 6101000, 6098000, 6935000, 8644000, 757…

## $ France <dbl> 4861000, 5465000, 8440000, 8223000, 9706000, 8809000, 806…

## $ Sweden <dbl> 10723000, 12333000, 23562000, 30595000, 46253000, 3886900…

## $ China <dbl> 8103000, 4040000, 25974000, 34776000, 31125000, 31576000,…

Im “tidy”-Style werden die Daten im Long-Format benötigt. Wir nutzen die “pivot_longer” Funktion. Anschliessend konvertieren wir das tibble-Objekt (= tidy dataframe) in ein tsibble Objekt, welches ein dataframe für Zeitreihen ist.

prep_data = raw_data %>%

pivot_longer(., cols = 2:9, names_to = "Subsidiary", values_to = "Revenues") %>%

mutate(Month = yearmonth(Month)) %>%

tsibble(., key = Subsidiary, index = Month)

glimpse(prep_data)

## Rows: 808

## Columns: 3

## Key: Subsidiary [8]

## $ Month <mth> 2011 Jan, 2011 Feb, 2011 Mar, 2011 Apr, 2011 May, 2011 Jun…

## $ Subsidiary <chr> "Austria", "Austria", "Austria", "Austria", "Austria", "Au…

## $ Revenues <dbl> 1436000, 2390000, 6556000, 7544000, 9069000, 8154000, 8173…

To get a feel for the data, let's look at it first.

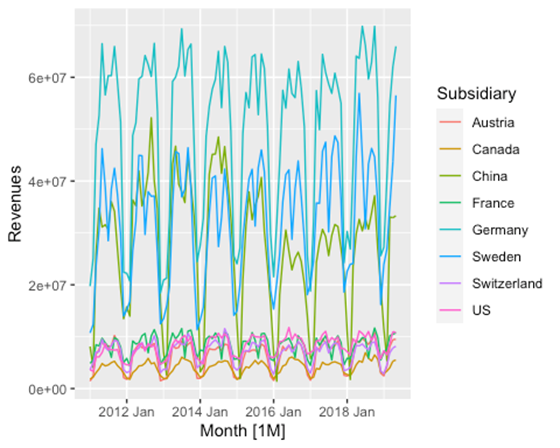

prep_data %>% autoplot(Revenues)

We see that there is a break in the data between 2016 and early 2020. After consulting with the technical expert, we know that it is a system change and all values must be non-negative. We correct this.

prep_data = prep_data %>%

mutate(Revenues = abs(Revenues))

prep_data %>% autoplot(Revenues)

It can now be seen that the available time series have a strong seasonal character. The data are thus prepared and can be modelled.

Modelling the time series analysis

Two widely used models available in the Fable package are ETS and ARIMA. These models are specified with a compact formula representation. The response variable (Revenues) and all transformations are included on the left-hand side, while the model specification is on the right-hand side of the formula. If a model is not fully specified (or if the right-hand side of the formula is completely missing), the non-specified components are automatically selected.

We use both model classes to find the best model for the respective time series.

fit <- prep_data %>%

model(

ets = ETS(Revenues),

arima = ARIMA(Revenues)

)

## Warning in sqrt(diag(best$var.coef)): NaNs produced

With coef() one can access all fit parameters of a model.

fit %>% coef()

## # A tibble: 145 x 7

## Subsidiary .model term estimate std.error statistic p.value

## <chr> <chr> <chr> <dbl> <dbl> <dbl> <dbl>

## 1 Austria ets alpha 2.21e-1 NA NA NA

## 2 Austria ets gamma 1.00e-4 NA NA NA

## 3 Austria ets l 6.43e+6 NA NA NA

## 4 Austria ets s0 -4.15e+6 NA NA NA

## 5 Austria ets s1 -3.35e+5 NA NA NA

## 6 Austria ets s2 2.47e+6 NA NA NA

## 7 Austria ets s3 2.42e+6 NA NA NA

## 8 Austria ets s4 1.35e+6 NA NA NA

## 9 Austria ets s5 1.78e+6 NA NA NA

## 10 Austria ets s6 1.82e+6 NA NA NA

## # … with 135 more rows

With glance, various statistical parameters of the fit of the model to the time series can be viewed.

fit %>% glance

## # A tibble: 16 x 12

## Subsidiary .model sigma2 log_lik AIC AICc BIC MSE AMSE

## <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 Austria ets 3.51e+11 -1568. 3166. 3172. 3205. 3.02e11 3.14e11

## 2 Canada ets 1.08e- 2 -1529. 3088. 3093. 3127. 1.47e11 1.53e11

## 3 China ets 1.84e+13 -1768. 3566. 3572. 3605. 1.59e13 2.76e13

## 4 France ets 5.57e+11 -1591. 3213. 3218. 3252. 4.80e11 4.79e11

## 5 Germany ets 1.98e+13 -1772. 3573. 3579. 3613. 1.71e13 1.73e13

## 6 Sweden ets 1.08e+13 -1741. 3512. 3517. 3551. 9.26e12 1.02e13

## 7 Switzerla… ets 3.61e+11 -1569. 3169. 3175. 3208. 3.11e11 3.20e11

## 8 US ets 5.81e- 3 -1568. 3172. 3181. 3219. 3.20e11 3.23e11

## 9 Austria arima 4.55e+11 -1308. 2624. 2625. 2634. NA NA

## 10 Canada arima 1.82e+11 -1285. 2581. 2582. 2593. NA NA

## 11 China arima 2.07e+13 -1492. 2992. 2992. 3002. NA NA

## 12 France arima 5.13e+11 -1329. 2672. 2674. 2690. NA NA

## 13 Germany arima 2.20e+13 -1498. 3003. 3003. 3010. NA NA

## 14 Sweden arima 1.10e+13 -1468. 2944. 2944. 2954. NA NA

## 15 Switzerla… arima 4.56e+11 -1322. 2655. 2655. 2667. NA NA

## 16 US arima 4.78e+11 -1311. 2633. 2634. 2648. NA NA

## # … with 3 more variables: MAE <dbl>, ar_roots <list>, ma_roots <list>

With the forecast function we generate the forecasts for each time series from the models.

fc = fit %>%

forecast(h = "2 years")

Finally, we visualize the forecasts. It can be seen that both methods pick up the patterns of the individual time series and incorporate them into the forecast of their respective methodology, as is the case, for example, with the "summer slump" in the French subsidiary or the rising trend in the US company.

fc %>% autoplot(prep_data) +

ggtitle("Reveunes of Company's Subsidiaries")

Download Wiki article as a .pdf

Know more?

Would you like to delve deeper into this topic? Then we would be happy to talk to you personally about the areas of application of R - gladly also in connection with analytics products from SAP. Simply get in touch with us!

Published by:

Dr. Stefan Lieder

Former Head of Data Science Workshop

Dr. Stefan Lieder

How did you like the article?

How helpful was this post?

Click on a star to rate!

Average rating 0 / 5.

Number of ratings: 0

No votes so far! Be the first person to rate this post!